Discover what ION can do for you

About IT2

Treasury is all about control. When expanding operations stretch existing processes their limits, Treasury teams need to rethink applying automation to support their organizations. IT2 is a comprehensive treasury and risk management solution that puts process control back into the hands of the treasury team. It’s built to serve the comprehensive needs of international treasury operations, providing an integrated framework for treasury policy, processes, and performance in an interactive and easy-to-use package.

Why IT2?

IT2 is a treasury solution that gives teams the tools they need to define the organization they envision. Integrated process maps, workbenches and dashboards help teams manage workflows for cash and liquidity, funding and assets, exposures, and accounting.

Get global cash visibility for optimal cash and liquidity management.

Get support for deal capture and lifecycle events for instruments across all asset classes.

Manage FX, investments, debt, credit facilities, intercompany loans, and deals efficiently.

Automate hedge effectiveness testing, journal creation, and journal export to the GL.

Intercompany account structures, multi-lateral netting, and automated cash pooling.

Highly configurable workbenches and dashboards for reporting.

Key features

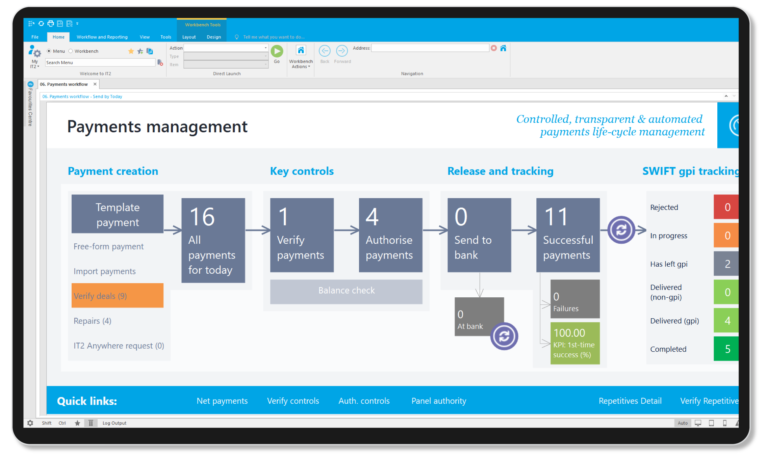

Unique process-based user experience

Unique visual process maps provide complete visibility of all workflows.

Process maps feature real-time task counts, so you always know what to do and when.

Process-based workflows give you unparalleled transparency and control.

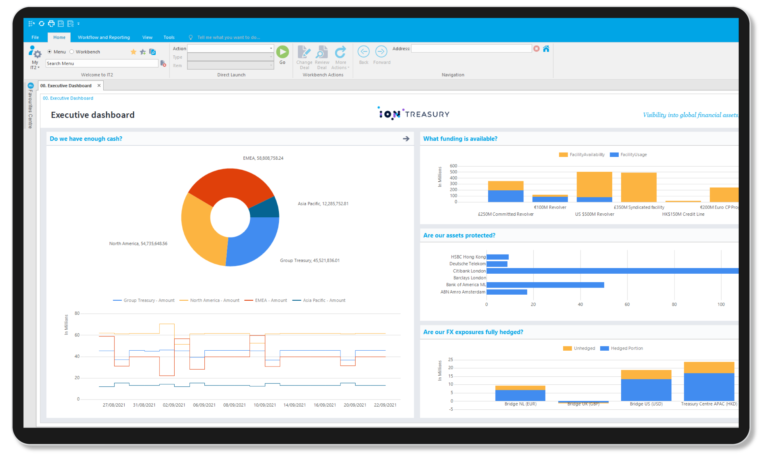

Reporting reimagined

Reports and charts from across IT2 can be easily combined into powerful, real-time dashboards.

Use the intuitive drag-and-drop interface to collect your data.

Native dashboarding allows a comprehensive view across treasury and benchmarking against KPIs.

Integration with any system, in any format

A native transformation engine handles integration with any system, in any format.

Integration through IT2´s own REST APIs, third-party APIs, or traditional file-exchange.

Access on-the-go from any device through IT2 Anywhere.

Enhance your solution with value added modules

At ION Treasury, we innovate at scale. We build new innovative tools once and roll them out to our entire product portfolio, offering cutting-edge technology to all ION Treasury customers. Our latest innovations include solutions for bank account management with bank fee analysis, money market funds, machine learning, and mobile treasury.

IBAM

Web-based bank account management with bank fee analysis capabilities enabling users to maintain a centralized, accurate inventory of all bank accounts and bank documentation.

Machine learning

Enhanced capabilities powered by artificial intelligence and machine learning. Fast, accurate algorithms optimize the potential of your data to deliver new insights.

Money market funds

A seamless money market funds experience enabling full automation of the trade lifecycle. Real-time consolidated investment and cash reporting, and access to a rich set of money market fund data and analytics.

Treasury Anywhere

Access information from your ION treasury management system anywhere using any mobile device, tablet, laptop, or PC.

Latest Treasury awards

RiskTech100 2024

IDC MarketScape 2023 Vendor Assessment

Stevie Awards 2023

Central Banking’s Awards 2023

Related products

City Financials

A pre-configured treasury and risk management solution that provides efficiency and strong controls using standard treasury practices.

Openlink

A comprehensive enterprise treasury and risk management solution for large commodity-intensive organizations needing extensive asset class coverage.

Reval

A highly scalable, comprehensive, and integrated treasury and risk management SaaS solution.

Wallstreet Suite

An enterprise treasury and risk management solution designed for the unique needs of the world’s largest, most complex organizations.